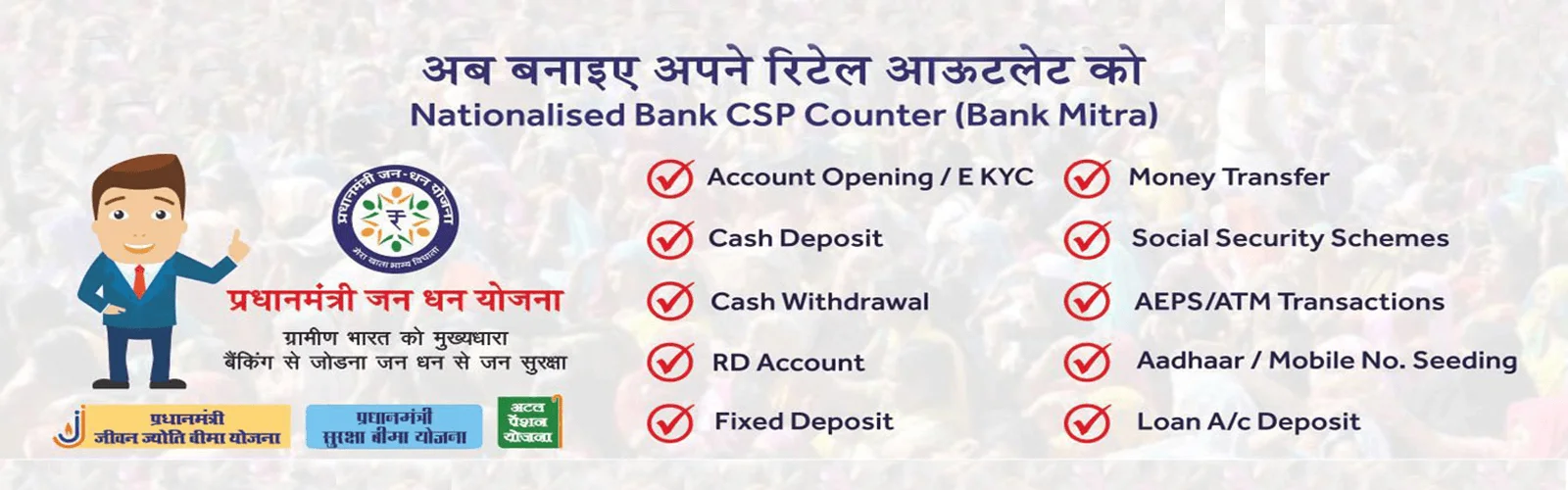

The Pradhan Mantri Jan Dhan Yojana (PMJDY) is a financial inclusion initiative launched by the Government of

India on August 28, 2014. The primary aim of the scheme is to provide affordable access to financial services

such as bank accounts, remittances, credit, insurance, and pensions to the unbanked population of India. Here

are the key details of the scheme:

Objectives

- Financial Inclusion: To ensure access to financial services, particularly by opening bank

accounts for those who do not have one.

- Direct Benefit Transfers (DBT): To facilitate direct transfers of subsidies and benefits

from various government schemes to the beneficiaries' bank accounts.

- Social Security: To provide financial security and support to the economically weaker

sections of society.

Key Features

-

Zero Balance Account:

- Accounts can be opened with zero balance.

- However, if the account-holder wishes to receive a checkbook, they must maintain a minimum balance.

-

RuPay Debit Card:

- Account holders receive a RuPay debit card that provides accidental insurance cover of ₹1 lakh.

- For accounts opened after August 28, 2018, the accidental insurance cover has been doubled to ₹2

lakh.

-

Overdraft Facility:

- An overdraft facility of up to ₹10,000 is available for account holders who have operated their

accounts satisfactorily for six months.

- Initially, an overdraft of ₹5,000 is allowed, which can be increased based on account performance.

-

Life Insurance Cover:

- Account holders are provided with a life insurance cover of ₹30,000, payable on death if the account

was opened between August 15, 2014, and January 26, 2015.

-

Simplified KYC Process:

- The Know Your Customer (KYC) process has been simplified to allow easy opening of accounts.

-

Mobile Banking:

- The scheme facilitates mobile banking through basic feature phones, enabling account holders to

check their balance and transfer funds.

-

Direct Benefit Transfers (DBT):

- The government utilizes these accounts for the transfer of subsidies and other financial benefits

under various schemes.

Achievements

- Widespread Inclusion: As of 2024, the scheme has led to the opening of over 50 crore bank

accounts.

- Balance and Deposits: These accounts hold significant deposits, contributing to the savings

culture in the country.

- Women Empowerment: A significant proportion of accounts are held by women, contributing to

financial empowerment.

- Insurance and Pension: The scheme has provided millions of people with access to insurance

and pension schemes.

How to Open a Jan Dhan Account

- Eligibility: Any Indian citizen above the age of 10 is eligible to open a Jan Dhan account.

- Documents Required: Basic KYC documents such as an Aadhaar card, PAN card, or any other

government-issued ID.

- Where to Apply: Jan Dhan accounts can be opened at any bank branch or through banking

correspondents.

Significance

- Empowering the Poor: PMJDY has played a crucial role in empowering the economically weaker

sections of society by integrating them into the formal financial system.

- Boost to Digital Payments: The scheme has significantly contributed to the rise in digital

transactions in India, especially post-demonetization and during the COVID-19 pandemic.

Overall, the Pradhan Mantri Jan Dhan Yojana is a landmark initiative in India's financial inclusion efforts,

bringing millions of unbanked citizens into the formal banking system and providing them with financial security

and access to various government benefits.